| Plastics Markets: The Road Ahead |

| by Dr. Peter Mooney |

| Trends Winter 2010 |

|

Over the past few years, the U.S. economy has encountered the most serious downturn in overall economic activity since the Great Depression, resulting in destructive repercussions throughout Wall Street and Main Street. As we slowly, tentatively emerge from this cathartic experience, embarking upon a new year and a new decade, plastics industry participants resin, additive, and machinery manufacturers; plastics processors; compounders; tool-makers; et al. are scanning the horizon for markets that can help them regain their former growth dynamic. Should they rely on traditional markets or should they instead explore new niche markets, those driven by recent material and processing innovations? As these companies strategize, it behooves them to briefly look back before attempting to visualize what is ahead. The past is not necessarily prologue to the future. Nonetheless, it can confirm where weve been and provide insight as to where we may be heading.

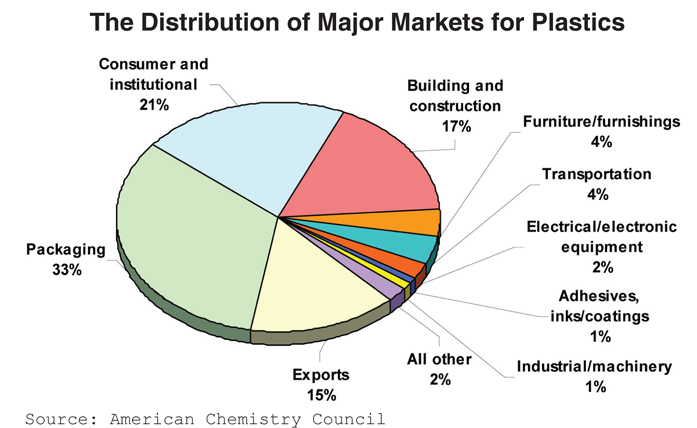

Over the past decade the major markets for U.S. plastics processors have been those portrayed in the graphic below. Packaging constitutes 33 percent of the total market. Packaging is unique insofar as it is relatively recession-resistant. Industrial production may rise and fall, yet the demand for plastic material (e.g., blow molded bottles, extruded film bags, thermoformed clam-shells) used in packaging food and non-food products hardly fluctuates. The same is true of medical equipment, which is subsumed in the all other category. By contrast, the demand for durable manufactured goods (e.g., automobiles, electronic equipment, residential and office furniture) tends to correlate closely with the upswings and downswings of the business cycle.

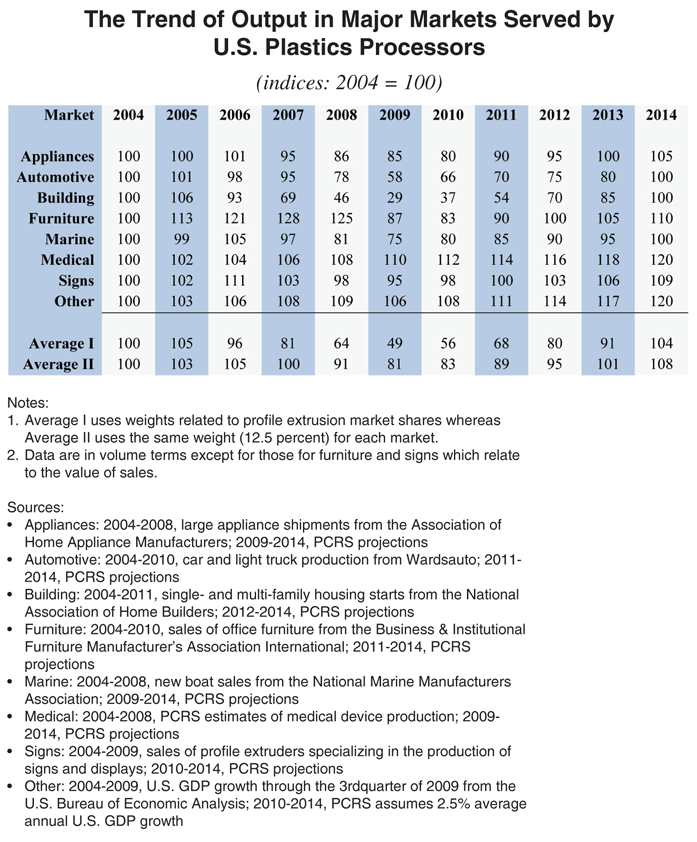

How have these markets fared over the recent past, and how are they likely to fare in the near-term future? In December 2009, I published a new multi-client report covering the North American profile extrusion business. As part of that research program, I gathered data from industry associations tracking developments in the major markets served by these processors. These organizations have collected and disseminated data relating to the trend in the volume of output in their respective markets over the time period 2004-2008. Some also have generated forecasts for 2009, 2010, and in some cases 2011. I extrapolated from their data and projections to extend the time frame out to 2014 in the table on page 25.

Obviously, many other plastics processors injection molders, compression molders, rotomolders, industrial blow molders, industrial thermoformers, et al. have customers in these structural part markets. Thus there are two averages at the bottom of the table Average I weighted by market shares specific to profile extruders and Average II where each market is accorded the same weight (12.5 percent). This table can be read to project the length of time required for profile extruders and other structural plastic part processors to regain the volume of output attained in their major markets in 2004. Some of these markets (e.g., medical equipment, other) will have experienced sustained growth over this entire 10-year period. Others (e.g., signs and displays, furniture) experienced relatively moderate pullbacks in 2008 and 2009, and full recovery is anticipated by 2011 or 2012. Still others (e.g., automotive, building and construction, and marine products) suffered deep demand erosion as a result of the recession, and they will only regain their 2004 volume of output by 2014. For structural plastics processors as a whole this exercise suggests that overall recovery will be regained by 2013. At first blush the scenario portrayed in this table is daunting. However, facts (i.e., the data for 2004-2008) are stubborn things. As the late, great Senator from the state of New York, Daniel Patrick Moynihan, once intoned, Everyone is entitled to their own opinion, but not their own facts. The fact of the matter is that the volume of output of this composite of markets served by profile extruders and other structural plastic part processors declined for 3-4 years (from 2005-2006 to 2009). It is entirely plausible that full recovery may take 3-5 years. The chairman of the Federal Reserve Board alluded to this prospect, recently suggesting full recovery in the U.S. labor market may take 5-6 years. The chief economist at DuPont also concurs; he believes recent data relating to U.S. output and employment do not imply a rapid return to pre-recession peaks. How about new niche markets? To what extent can they supplement lost sales in traditional structural plastic part markets? In the presentation I made to the MAPP Benchmarking & Best Practices Conference in October 2009, I alluded to several recent breakthrough technologies in plastic materials and processing namely bioplastics, inherently conductive plastics, in-mold labeling and micro-molding, nanotechnology, and fully-automated rotational molding. I also alluded to markets ripe for plastic material and processing innovations alternative energy, electric vehicles, mass transit, and medical devices. So the plastics industry doesnt lack for opportunities to recharge its former growth dynamic. At the conclusion of my presentation, I indicated that as a card-carrying economist I am frequently asked whether the recovery of the U.S. economy will be V-shaped, W-shaped, U-shaped, or L-shaped. I noted that one year ago we were all afraid that the future path of the economy would be I-shaped that is, straight down! Those fears are by now completely dispelled. U.S. real GDP rose at an annual 2.8 percent rate in the third quarter of 2009, and the consensus expectation among economists inside and outside of government is that growth in the fourth quarter will be 3.5 percent or higher. Manufacturing industry output has been growing since August 2009, according to the Institute for Supply Management (ISM). These data point to the inherent recuperative powers of the U.S. economy (if only the federal government and Congress can resist strangling it through excessive regulation and costly healthcare reform). Yet this is no time for plastics industry participants to stand idly by, waiting for the rising tide to lift all boats. The business mantra of the moment is innovation. It is axiomatic for both countries and companies that the only way to build wealth and create jobs is through productivity improvements that come from investment and innovation. As we enter the new decade, plastics processors need to review every aspect of their internal operations. They need to spend time not only reconnecting with existing customers in traditional markets, but also exploring new markets. They need to be risk-takers. They need to re-evaluate their business models to ensure they are appropriate for the new normal economy of the future. They need to consider diversifying their processing capabilities so if a customer brings a part that really should be blow molded or injection molded or rotomolded or thermoformed, they can supply that part. Above all they need to devote the time and resources required to track innovations, emanating from any and every quarter, that can improve their operations. The stage of cost-cutting is over. It will be the truly innovative, risk-taking processors that will survive and thrive in the reset economy of the future. Dr. Peter J. Mooney is president of Plastics Custom Research Services of Advance, N.C. and one of the plastics industrys foremost economic research experts on evolving domestic and global plastics industry market opportunities. Visit the Plastics Custom Research Services website at www.plasres.com. |